An allowance, when done correctly, can be the perfect way to solidify financial literacy at an early age.

It can teach them the value of a dollar, budgeting and prioritization in a way that is fun and engaging. But what’s the right way to give a kid an allowance so it is meaningful and not just a weekly expectation?

Here are 14 ways to ensure your kid’s allowance is meaningful.

Types of Allowances

You’re all set to give your kiddo an allowance, so you should just do like your parents did, right? Well, that all depends on how your parents handled allowances.

According to Karyn Hodgens, a personal finance educator who works with children, there are two main schools of thought when it comes to allowances: paying for chores or using an allowance as a teaching instrument.

Chore-based allowances are what most of today’s parents were brought up with. We washed the dishes, cleaned our rooms, mowed the grass, etc., and our parents would hand us a crisp $5 bill when we went to the mall or movies on a Friday night. When you use an allowance as an education tool, you treat the money you give your kids as practice money instead of forcing them to earn it.

According to Hodgens, both approaches teach important lessons, but one method is superior to the other.

Which Allowance Type Is Right?

Hodgens points to the self-determination theory as the key to success in giving an allowance. Sure, an allowance tied to chores does have some value, as it teaches the child the relationship between work and money.

While that is valuable, Hodgens says, “the sense of autonomy is lost along with the interest in completing the tasks” because the kid is now forced to do chores to get an allowance. A sense of autonomy is one of the keys to being intrinsically motivated, which is when motivation comes from inside instead of from an outside motivator, like money.

The likely result is that eventually the child won’t feel like doing the chores or feel that the money given for the chores is no longer sufficient and will simply stop doing them. And this could produce a power struggle between the parents and the child.

Tying a regular allowance to learning about money is a better route. But there are caveats to this preferred style of allowance giving.

Setting Expectations

I know what you’re thinking, “Wait, so I am supposed to just hand my kid money for nothing?” No. Hodgens explains that this type of allowance is counterproductive and can create an entitled kid who thinks they get everything handed to them.

Instead, Hodgens recommends parents and kids sit down and speak about the expectations attached to this allowance. They should include budgeting, spending responsibilities and appropriate compensation. This compounds the learning process and builds what she calls a task-noncontingent reward, which is a reward that’s not specifically attached to a task. Instead, the reward is the learning, and the allowance simply enables this learning.

But why would any kid see learning as a reward? According to Hodgens, children seek for competence, and learning an “adult thing” like money is a huge step for them.

Use this innate desire to learn to your advantage.

Daily Chores Still Exist

So, if we’re not tying daily chores to cash, how do we get things done around the house? This one is simple: Everyone has a job to do.

Being a productive member of the household is something that a parent needs to instill early in life. My 7-year-old, for example, is responsible for putting his own clothes in the laundry and cleaning his room sans pay. And he will soon take on more responsibilities as his capacities (and height) allow.

According to Hodgens, “Having kids share in the responsibility of running an efficient household taps into their psychological need to be connected to others.”

This makes them feel good about helping around the house and turns that connection into the intrinsic motivation to continue doing it for free.

They Can Learn by Earning, Too

While we shouldn’t pay kids for daily chores, there are times when this is perfectly fine.

Hodgens calls these the “above-and-beyond jobs.” These are the chores that might hire someone to do. Instead, you can offer to pay your child to complete them. These are things like mowing the grass, washing the car, painting the fence or weeding the garden.

Sit down with your child and talk about the jobs they would want to do for extra money and what would be appropriate compensation for each task.

The child is not required to do any of these chores, but if they want extra money, they will have to either save their regular allowance or do some of these extra jobs.

This teaches them the relationship of work and money without tying normal around-the-house items to money.

Combining Power Works for Some

Denise Cummins, psychologist and author, took an interesting approach with her children, combining methods to create a balance that resulted in “precious few arguments about money.”

She gave her kids normal chores around the house and tied them to a base $10 allowance. In addition to that, she offered them bonus chores that they could do on an as-needed basis. This gave the kids a normal flow of money to work with and learn from, but it also taught them the value of working harder to earn more money.

If one of her kids decided they wanted a pricey toy, they could either save up their normal allowance or use the above-and-beyond jobs to fill the gap.

The Art of Saving

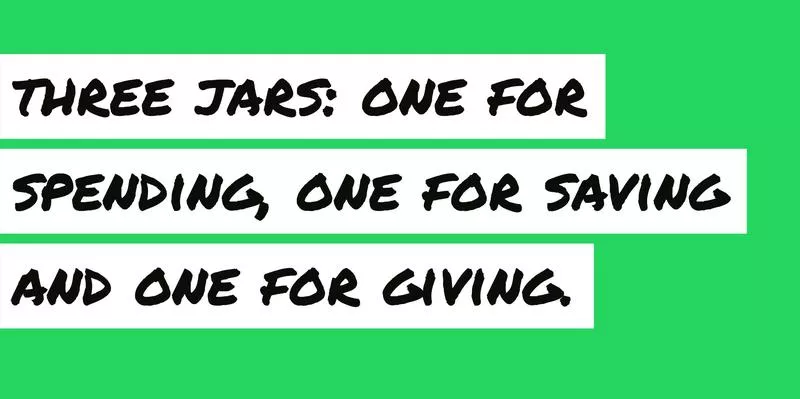

While adults generally understand the need to save, kids see money as a means to buying things. This is where parents can use an allowance to guide their kids. Cummins mentions the three-jar method, which is a widely used method of early budgeting.

How it works is you lay out three jars: one labeled “spending,” one labeled “saving” and one labeled “giving.” Then have your child split their allowance evenly in those three jars. Some parents prefer a two-jar method, which includes just spending and saving, but the general concept is the same.

This not only teaches your child the very basics of budgeting, but it also shows them the power of saving. At the end of the year, your child may have a relatively large amount of money saved that they can spend on something they’ve been eyeing for a while or roll it over into the next year.

Raffi Bilek, a social worker with Baltimore Therapy Center agrees with this method, stating, “Having children practice distributing their money responsibly and with an eye to the needs of others is a great way to help them develop a good relationship with money as adults.”

Cummins increased the power of this method by installing compounding interest on her kids’ savings. As her kids left their savings untouched, Cummins gave them 5 percent interest compounded daily. This not only taught them the power of saving, but it also incentivized it by giving them interest.

Let Them Spend It

As adults, we should know that we need to budget and set aside money for discretionary spending. This is something that kids, who’ve never paid a bill in their lives, may have no idea about. So, this is where that meaningful allowance really takes hold.

Some parents may think forcing their own budgeting schemes upon their child is the best way to teach them. But that takes away the all-important autonomy of the process.

According to Hodgens, giving them “personal control over what happens to that money” makes the learning process more exciting and meaningful for children than just being handed a list of chores and few bucks.

Of course, you have to regulate a little, but if little Suzie wants to use the money from her “spending” jar to buy that stuffed animal now, you should let her — it’s her money, after all.

Money as a Learning Tool

As parents, we all know that kids generally want everything, and we work as the filter because we’re the ones paying for it. While this is a great way to keep kids from draining your bank account, it only teaches them that mommy and daddy always say “No.”

With their own money, they are free to buy nearly anything that fits their budget, but it also teaches them to spend wisely.

So, let’s say Suzie bought that stuffed animal on impulse. She gets it home, plays with it for five or 10 minutes, then never plays with it again. Then, a week later, she sees her favorite doll is on sale, and it would have fit her allowance budget perfectly had she not spent it on her forgotten stuffed animal.

Right then, she learns a key money lesson: delay of gratification. Because Suzie learned this lesson in a context that she can relate to and is passionate about, it is more likely to stick with her in the long run.

Her response may be tears, but it is your job as a parent to sit her down and explain this important lesson. At this point, that complex money lesson is something she can understand.

Drawing Up a Fair Allowance

Sometimes, coming up with an allowance amount is the hardest part of the whole process. Just how much is enough? The key is to make it so your kids are self-sufficient. This means their allowance covers all their basic needs and their extra-curricular activities.

So, sit down and look at all your weekly and monthly expenditures related to your kiddos. Add in everything: clubs, after-school activities, sports dues, lunch money, movie tickets, etc.

Once you have that number figured out, add a little on top for random treats here and there, and present that amount as their allowance.

Budgeting 101

Phycologist Marie Hartwell-Walker recommends setting a budget with your kids. Their budget will determine what they can actually afford.

If your child goes over their budget and cannot afford something, then tell them they need to wait until their next “paycheck” comes before they can get more money.

This may mean they have to skip the movies one week or miss out on that pizza party, but it teaches them a valuable lesson about staying within their budget and prioritizing their expenses.

Regular Financial Check-Ins

Like most things in parenting, an allowance is far from a set-it-and-forget-it duty. You can’t walk your child through earning an allowance, budgeting and saving, and expect them to be a savant.

They need regular check-ins to make sure things are going well and discuss any roadblocks they’ve encountered.

Hartwell-Walker recommends having weekly meetings about money, especially in the beginning. During these meetings, avoid being critical or scolding if your child has struggled. Use these as teaching moments and praise them for what they have succeeded in.

Stepping Up the Responsibilities

To grow financial literacy, slowly increase your child’s responsibility in dealing with their allowance.

For example, your 8-year-old will likely only get the bare-bones budgeting lessons from using their allowance on fun things. Your 15-year-old, however, may also get an additional bonus of sorts to handle back-to-school shopping, according to Hartwell-Walker.

Letting your 15-year-old see just how much those designer jeans eat into their budget could make them think twice about buying them instead of two pairs of cheaper jeans. This could also breed more resourcefulness, as they may discover the art of discount shopping to get the brand names at a lower price.

They may come up short on clothes for school because they overspent on high-end items, but insist they get by and use their regular allowance to buy additional clothes over time.

Be a Great Role Model

We can advise our children with money, but the best way for them to learn good financial practices is seeing us exercising good financial practices.

Make sure you treat your salary like an allowance and follow all the same advice you give your children. If they question a decision you made, address it honestly, even if they busted you making a bad financial move.

You never know, maybe you can learn a thing or two from your kids.